Chapter 5: Making Your Money Work For You

Key Terms

Investing - Allocating resources with the expectation of generating returns or income over time.

Saving - Setting aside income for future use or emergencies.

Stock - Ownership in a corporation, representing a share of its assets and earnings.

Bond - A debt security representing a loan made by an investor to a borrower (typically corporate or governmental) for a defined period, with fixed or variable interest payments.

Asset Allocation - Distribution of investments across various asset classes to manage risk and achieve financial goals.

Speculating - Engaging in risky financial transactions with the expectation of significant short-term gains.

Diversification - Spreading investments across different assets to reduce risk exposure.

Financial Professionals - Individuals or firms providing financial advice, planning, and management services.

Two Ways To Make Money

(Office of Investor Education and Advocacy Securities and Exchange Commission, 2015)

There are basically two ways to make money.

You work for money - Someone pays you to work for them or you have your own business.

Your money works for you - You take your money and you save or invest it.

Your Money Can Work For You In Two Ways

Your money earns money - When your money goes to work, it may earn a steady paycheck. Someone pays you to use your money for a period of time. When you get your money back, you get it back plus “interest.” Or, if you buy stock in a company that pays “dividends” to shareholders, the company may pay you a portion of its earnings on a regular basis. Your money can make an “income,” just like you. You can make more money when you and your money work.

You buy something with your money that could increase in value - You become an owner of something that you hope increases in value over time. When you need your money back, you sell it, hoping someone else will pay you more for it. For instance, you buy a piece of land thinking it will increase in value as more businesses or people move into your town. You expect to sell the land in five, ten, or twenty years when someone will buy it from you for a lot more money than you paid. And sometimes, your money can do both at the same time— earn a steady paycheck and increase in value.

Investing

(The Church of Jesus Christ of Latter-day Saints, 2017)

When people hear the term investing, they may think of a loud and chaotic trading floor with people selling stocks and bonds. While that may be part of investing, investing is also the act of putting time, effort, or money into something and expecting some type of a return.

Simply Save

One of the easiest ways to invest is to save money. You have been working to build an emergency fund, starting with one month’s worth of expenses and then building up to having three to six months’ worth of expenses. Imagine the possibilities if you continue to save even after establishing a strong emergency fund.

Elder L. Tom Perry taught, “Pay yourself a predetermined amount directly into savings. … It is amazing to me that so many people work all of their lives for the grocer, the landlord, the power company, the automobile salesman, and the bank, and yet think so little of their own efforts that they pay themselves nothing” (Perry, 1991).

(Office of Investor Education and Advocacy Securities and Exchange Commission, 2015)

Your savings are usually put into the safest places, or products, that allow you access to your money at any time. Savings products include savings accounts, checking accounts, and certificates of deposit. In the U.S., some deposits in these products may be insured by the Federal Deposit Insurance Corporation or the National Credit Union Administration. But there’s a tradeoff for security and ready availability. Your money is paid a low wage as it works for you.

After paying off credit cards or other high-interest debt, most smart investors put enough money in a savings product to cover an emergency, like sudden unemployment. Some make sure they have up to six months of their income in savings so that they know it will absolutely be there for them when they need it.

But how “safe” is a savings account if you leave all of your money there for a long time, and the interest it earns doesn’t keep up with inflation? Inflation is the increase in the general price of goods and services over a period of time.

Think back to when you were a young child. How much did your favorite candy cost back then? How much does that same candy cost today? It likely costs more today than it did when you were younger. This is due to inflation. This is why many people put some of their money in savings, but look to investing so they can earn more over long periods of time, say three years or longer.

Education

(The Church of Jesus Christ of Latter-day Saints, 2017)

Education is another form of investing. Typically, additional training or education will have a cost. If you are going to invest in education, ensure that it will lead to better work so there is a good return on your investment.

President Gordon B. Hinckley counseled that the “world will in large measure pay you what it thinks you are worth, and your worth will increase as you gain education and proficiency in your chosen field” (Hinckley, 2001).

Sometimes it may be appropriate to incur debt to gain education, but there are also many other ways to pay for school. Explore all other options before turning to debt. If you do go into debt for education, strive to pay it off as quickly as possible.

Investing

(The Office of Financial Readiness, 2020)

Stocks, bonds, bears, bulls — making your way through investing buzzwords can be confusing. Let’s start with a basic understanding of investing. In simple terms, investing is using money to try to make a profit or produce income. Investing money is different from saving money. Saving involves setting money aside in safe, relatively low-interest paying accounts so it’s there when you need it. Investing is about taking calculated risks with your money to try to earn more with it. Most people invest to achieve a goal, whether it be a long-term goal like retirement or a short-term goal like saving for a down payment on a house.

Why Should I Invest?

Even with the potential benefits of investing, it’s important to understand that you could lose money doing it. Given the fact that you’re not guaranteed to make more than if you saved your money, why invest at all?

Here are 3 good reasons why:

Potential for Higher Returns - Investing gives you the chance to earn higher returns. The larger your returns, the more money you’ll have in the future.

Achieving Long-Term Goals - Savings alone might not allow you to accumulate enough to reach your goals. Investing those same dollars can increase those chances, or at least position you to accumulate more money over time.

Inflation - Inflation affects goals that are years in the future. Expect things to cost more in the future than they do today. Investing offers the potential to keep up with – and even outpace – inflation.

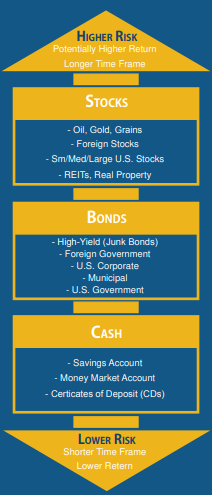

Types of Investments

Stocks

A stock — also known as a share or equity — is a type of investment representing ownership in a company. Companies sell stock to raise money to fund their business. You become a shareholder and own part of the company when you buy stock. As a shareholder, you share in the company’s profits if it chooses to distribute periodic payments called dividends.

If the company is successful, then the stock may become more valuable and can be sold for a profit. On the other hand, if the company has problems, then the shares in the company might become less valuable or become completely worthless, and an investor can lose money from the original investment.

Bonds

A bond is an investment representing a loan made by an investor to a borrower — typically a business or government entity. The borrower promises the debt will be paid back with interest at a specific time. Bonds are typically issued by companies, municipalities, states, and sovereign governments to finance projects and operations.

Cash

Cash and cash equivalents such as savings accounts, money markets, and certificates of deposit (CDs) are intended to be relatively safe and accessible. They tend to offer relatively low yields and returns because there’s not as much risk associated with these products, like with stocks or bonds. This typically makes cash and cash equivalent products a poor choice for long-term goals because many of them won’t even keep up with inflation.

Why Some Investments Make Money And Others Don’t

(Office of Investor Education and Advocacy Securities and Exchange Commission, 2015)

You can potentially make money in an investment if:

The company performs better than its competitors.

Other investors recognize it’s a good company so that when it comes time to sell your investment, others want to buy it.

The company makes profits, meaning they make enough money to pay you interest for your bond, or maybe dividends on your stock.

You can lose money if:

The company’s competitors are better than it is.

Consumers don’t want to buy the company’s products or services.

The company’s officers fail at managing the business well, they spend too much money, and their expenses are larger than their profits.

Other investors that you would need to sell to think the company’s stock is too expensive given its performance and future outlook.

The people running the company are dishonest. They use your money to buy homes, clothes, and vacations, instead of using your money on the business.

They lie about any aspect of the business: claim past or future profits that do not exist, claim it has contracts to sell its products when it doesn’t or make up fake numbers on its finances to dupe investors.

The brokers who sell the company’s stock manipulate the price so that it doesn’t reflect the true value of the company. After they pump up the price, these brokers dump the stock, the price falls, and investors lose their money.

For whatever reason, you have to sell your investment when the market is down.

Mutual Funds and Exchange Traded Funds (ETF)

(The Office of Financial Readiness, 2020)

If you think back to elementary school, you may remember learning about the three primary colors: red, yellow, and blue. You can create thousands of other colors by using these three colors as a foundation. This concept also works pretty well when you think of investing. Using the basic investments from above — cash, bonds, and stocks — you are able to create thousands of other investments.

Mutual Funds

(Office of Investor Education and Advocacy Securities and Exchange Commission, 2015)

A mutual fund is a pool of money run by a professional or group of professionals called the “investment adviser.” In a managed mutual fund, after investigating the prospects of many companies, the fund’s investment adviser will pick the stocks or bonds of companies and put them into a fund. Investors can buy shares of the fund, and their shares rise or fall in value as the values of the stocks and bonds in the fund rise and fall. Investors may typically pay a fee when they buy or sell their shares in the fund, and those fees in part pay the salaries and expenses of the professionals who manage the fund.

Exchange Traded Funds (ETF)

(The Office of Financial Readiness, 2020)

An ETF, or exchange-traded fund, is an investment that tracks a particular set of equities, similar to an index. It’s similar to a mutual fund but trades just as a normal stock would on an exchange, and its price adjusts throughout the day rather than at market close. ETFs can track stocks in a single industry, such as energy, or an entire index of equities like the S&P 500.

Funds Without Active Management

(Office of Investor Education and Advocacy Securities and Exchange Commission, 2015)

One way that investors can obtain for themselves nearly the full returns of the market is to invest in an “index fund.” This is a fund that does not attempt to pick and choose stocks of individual companies based upon the research of the mutual fund managers or to try to time the market’s movements. An index fund seeks to equal the returns of a major stock index, such as the Standard & Poor’s 500, the Wilshire 5000, or the Russell 3000. Through computer-programmed buying and selling, an index fund tracks the holdings of a chosen index, and so shows the same returns as an index minus, of course, the annual fees involved in running the fund. The fees for index mutual funds generally are much lower than the fees for managed mutual funds.

Historical data shows that index funds have, primarily because of their lower fees, enjoyed higher returns than the average managed mutual fund. But, like any investment, index funds involve risk.

Asset Allocation

(Office of Investor Education and Advocacy, 2009)

Asset allocation involves dividing an investment portfolio among different asset categories, such as stocks, bonds, and cash. The process of determining which mix of assets to hold in your portfolio is a very personal one. The asset allocation that works best for you at any given point in your life will depend largely on your time horizon and your ability to tolerate risk.

Time Horizon - Your time horizon is the expected number of months, years, or decades you will be investing to achieve a particular financial goal. An investor with a longer time horizon may feel more comfortable taking on a riskier, or more volatile, investment because he or she can wait out slow economic cycles and the inevitable ups and downs of our markets. By contrast, an investor saving up for a teenager's college education would likely take on less risk because he or she has a shorter time horizon.

Risk Tolerance - Risk tolerance is your ability and willingness to lose some or all of your original investment in exchange for greater potential returns. An aggressive investor, or one with a high-risk tolerance, is more likely to risk losing money in order to get better results. A conservative investor, or one with a low-risk tolerance, tends to favor investments that will preserve his or her original investment. In the words of the famous saying, conservative investors keep a "bird in the hand," while aggressive investors seek "two in the bush."

Risk vs Return

(Office of Investor Education and Advocacy, 2009)

When it comes to investing, risk and reward are inextricably entwined. You've probably heard the phrase "no pain, no gain" - those words come close to summing up the relationship between risk and reward. Don't let anyone tell you otherwise: All investments involve some degree of risk. If you intend to purchase securities - such as stocks, bonds, or mutual funds - it's important that you understand before you invest that you could lose some or all of your money.

The reward for taking on risk is the potential for a greater investment return. If you have a financial goal with a long time horizon, you are likely to make more money by carefully investing in asset categories with greater risk, like stocks or bonds, rather than restricting your investments to assets with less risk, like cash equivalents. On the other hand, investing solely in cash investments may be appropriate for short-term financial goals.

Why Asset Allocation Is So Important

(Office of Investor Education and Advocacy, 2009)

By including asset categories with investment returns that move up and down under different market conditions within a portfolio, an investor can protect against significant losses. Historically, the returns of the three major asset categories have not moved up and down at the same time. Market conditions that cause one asset category to do well often cause another asset category to have average or poor returns.

By investing in more than one asset category, you'll reduce the risk that you'll lose money and your portfolio's overall investment returns will have a smoother ride. If one asset category's investment return falls, you'll be in a position to counteract your losses in that asset category with better investment returns in another asset category.

In addition, asset allocation is important because it has a major impact on whether you will meet your financial goals. If you don't include enough risk in your portfolio, your investments may not earn a large enough return to meet your goal.

For example, if you are saving for a long-term goal, such as retirement or college, most financial experts agree that you will likely need to include at least some stock or stock mutual funds in your portfolio. On the other hand, if you include too much risk in your portfolio, the money for your goal may not be there when you need it. A portfolio heavily weighted in stock or stock mutual funds, for instance, would be inappropriate for a short-term goal, such as saving for a family's summer vacation.

What are the best investments for me?

(Office of Investor Education and Advocacy Securities and Exchange Commission, 2015)

The answer depends on when you will need the money, your goals, and if you will be able to sleep at night if you purchase a risky investment where you could lose your principal.

For instance, if you are saving for retirement, and you have 35 years before you retire, you may want to consider riskier investment products, knowing that if you stick to only the “savings” products or to less risky investment products, your money will grow too slowly—or, given inflation and taxes, you may lose the purchasing power of your money. A frequent mistake people make is putting money they will not need for a very long time in investments that pay a low amount of interest.

On the other hand, if you are saving for a short-term goal, five years or less, you don’t want to choose risky investments, because when it’s time to sell, you may have to take a loss. Since investments often move up and down in value rapidly, you want to make sure that you can wait and sell at the best possible time.

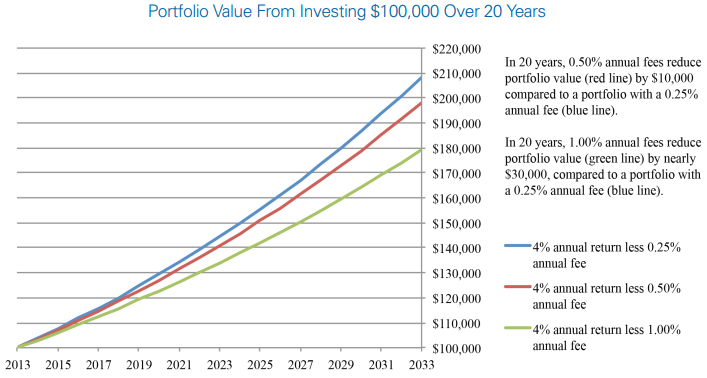

Fees

(Office of Investor Education and Advocacy, 2019)

As with anything you buy, there are fees and costs associated with investment products and services. These fees may seem small, but over time they can have a major impact on your investment portfolio. The following chart shows an investment portfolio with a 4% annual return over 20 years when the investment either has an ongoing fee of 0.25%, 0.50%, or 1%. Notice how the fees affect the investment portfolio over 20 years.

Along with the other factors you think about when choosing either a financial professional or a particular investment, be sure you understand and compare the fees you’ll be charged. It could save you a lot of money in the long run.

Investing vs Speculating

You may have heard of someone making a lot of money in a short period with some sort of investment. While this can happen, these stories should be taken with a grain of salt. Usually, in these instances, the individual could have lost just as much (if not more) than they initially invested and likely took higher risks for a higher reward. With this in mind, it is important to understand the difference between investing and speculating.

(ChatGPT, 2024)

Investing - Investing is a long-term strategy designed to build wealth over time. Investors typically have a lower tolerance for risk, aiming to preserve capital and achieve financial goals such as retirement or education.

Speculating - Speculation involves taking higher risks for the potential of short-term profits. Speculators have a higher tolerance for risk, accepting the possibility of significant losses in pursuit of potential high returns. Speculators typically have a shorter time horizon, seeking quick gains and frequently engaging in buying and selling within short time frames.

Strategies to Help with Investing

(The Office of Financial Readiness, 2020)

Invest Regularly

Invest a set amount of money regularly whether investment markets are moving up or down — a strategy known as dollar cost averaging. When prices are high, your regular contributions buy fewer shares (units of ownership in a company or mutual fund); when prices are low, your contributions buy more. This strategy tends to spread investment risk over time. Keep in mind that dollar-cost averaging does not ensure a profit or protect against loss in a declining market. Although dollar cost averaging will not protect you against losses when the stock or bond markets are declining, it does reduce your risk of investing by ensuring that stock and bond purchases are made at a variety of prices, buying more shares at lower prices and fewer at higher prices. Dollar-cost averaging also eliminates the risk of investing all of your money in the stock or bond market at market peaks. You should also consider your ability to invest continuously through periods when the market is down.

Invest for the Long Term

The more time you give your investment to grow and compound, the more likely you are to reach your financial goals. History shows that patient investors who focus on long-term goals can generally withstand fluctuations in the stock market. USE TIME, NOT TIMING. If you start early and invest regularly, you will likely be able to use time to your advantage. Do not try “timing” decisions to buy and sell based on market fluctuations. It is extremely difficult to predict the market fluctuations over the long term accurately.

Keep Emotions Out Of Your Actions

Investors’ decisions tend to be influenced by short-term variables and the latest news. Think and act intellectually, not emotionally. Investing success requires patience, determination, and an unemotional approach. Do your homework then stay on course. INCREASE YOUR KNOWLEDGE. Learn all you can about investing and specific investments by regularly reading reputable business periodicals, investment books, and annual reports of companies whose securities you might want to purchase. There is no shortage of opinion about investing and the market, be disciplined and use facts to guide your decisions.

Avoid High-Risk Investments

Avoid futures, commodities, and other risky forms of investing — at least until you have an established, diversified portfolio, you know all about them, and you are willing and able to accept their increased risks. Remember, you are investing, not speculating.

Avoid Chasing Performance

If you choose your investments by leaping into whatever is currently doing very well, you may be setting yourself up for recurring losses over time. Oftentimes, the best-performing stock in one year becomes one of the worst in subsequent years.

Diversification

Select a wide variety of securities for your portfolio to minimize investment risks. Investing in several unrelated assets will produce a return based on the average of your various investment returns, rather than relying completely upon the return of one investment.

(Office of Investor Education and Advocacy, 2009)

For example, have you ever noticed that street vendors often sell seemingly unrelated products - such as umbrellas and sunglasses? Initially, that may seem odd. After all, when would a person buy both items at the same time? Probably never - and that's the point. Street vendors know that when it's raining, it's easier to sell umbrellas but harder to sell sunglasses. And when it's sunny, the reverse is true. By selling both items- in other words, by diversifying the product line - the vendor can reduce the risk of losing money on any given day.

(The Office of Financial Readiness, 2020)

Evaluate Your Investment Plan

You should evaluate your investment plan at least annually or at times of significant life events. If necessary, rebalance your portfolio to ensure your mix of investments aligns with your goals, risk tolerance, and time horizon.

Stay Calm. Stick to Your Plan.

(Schock, n.d.)

If you have the right investment plan, you shouldn’t need to make rash decisions during times of market volatility. A plan that takes into account your long-term financial goals and risk tolerance and includes a portfolio of diverse assets, will better prepare you for inevitable market changes. Most importantly, whatever you do, don’t panic, plan it!

Financial Professionals

Sometimes investing can feel scary, intimidating, or confusing. There are a lot of emotions involved and the consequences can be steep. If you feel too overwhelmed or you simply don’t have the time, you could consider finding a financial professional to help. If you’re considering bringing on a financial advisor, below is some information to use during the selection process to help set you up for success.

(Calpers, 2023)

What type of financial services do they provide?

While retirement planning is the most notable planning assistance a financial advisor can provide, an advisor who gives guidance on other aspects of your finances is worth considering. Questions on budgeting, debt repayment, and insurance product suggestions are additional areas you may need to turn to them for. If you have a complex financial situation, these added services can serve as a great item to factor in during your selection process. However, if you’re single or don’t have significant debt, you might only need basic planning services.

Are they bound by a fiduciary duty?

Unfortunately, there aren’t regulations that outline the duties of a financial advisor. The U.S. Securities and Exchange Commission (SEC) is trying to change this, though, by only allowing the use of “advisor” to those who hold themselves to a fiduciary standard. Understanding if a financial advisor is obligated to a fiduciary duty is a crucial part of the selection process. This means they are legally required to work in your best financial interest.

In addition, it’s a good idea to find a financial advisor who is a certified financial planner (CFP), as they have in-depth financial planning knowledge and are always held to a fiduciary standard. CFPs are required to have several years’ experience in the financial planning field and must pass the CFP exam and adhere to strict ethical standards set by the Certified Financial Planner Board of Standards. You’ll find that some CFPs may specialize in specific areas like divorce or retirement planning, while others may choose to work with specific clients like small business owners or retirees.

Other advisors may only be held to a suitability standard, meaning they’ll suggest products that are suitable for you, but may be more expensive while also earning them a higher commission.

How do they earn their money?

There are two ways in which financial advisors earn their income. There are fee-only financial advisors who earn money from the fees you pay for their services. For example, you may be charged a percentage of the assets they manage for you, or you may be charged an hourly rate or even a flat rate. Typically, financial advisors who are paid in this manner are almost always fiduciaries.

There are also financial advisors who are commission-based. This means they earn their money from third parties, which is why they’ll advertise themselves as “free” because you aren’t charged a fee to use their services. If a financial advisor is commission-based, they aren’t fiduciaries but rather work in a sales capacity for investment and insurance brokerages.

Some financial advisors may even work as a combination of the two, such as those who offer advice on products like life insurance.

Watch Out for Red Flags

(Office of Investor Education and Advocacy, 2019)

Fraudsters use different means, including promotional videos, social media, email, phone conversations, and in-person meetings, to lure victims into scams. If it seems too good to be true, it probably is.

One of the most common gimmicks con artists use is to promise investors that they will make a lot of money in a short period of time – that they will “get rich quick.” Con artists may trick investors into believing that they will make tons of money with little or no effort (for example, for purchasing products or for performing trivial tasks, such as clicking on digital ads each day). This tactic often uses images of lavish lifestyles and luxury items to create the illusion of future riches (for example, wealth, fancy cars, mansions, yachts, vacations, etc.).

Check the background of anyone selling or offering you an investment and confirm that the person is currently registered or licensed. It only takes a few minutes using the free and simple search tools. Before you hand over any money or share your contact information, verify that the person is currently registered or licensed and find out if he or she has a disciplinary history.

(Office of Investor Education and Advocacy, 2021)

Regardless of whether someone claims to be registered with proper authorities, beware if you spot these warning signs of an investment scam:

Guaranteed High Investment Returns - Promises of high investment returns – often accompanied by a guarantee of little or no risk – is a classic sign of fraud. Every investment has risk, and the potential for high returns usually comes with high risk.

Unsolicited Offers - Unsolicited offers (you didn’t ask for it and don’t know the sender) to earn investment returns that seem “too good to be true” may be part of a scam.

Urgency - Con artists often claim an investment opportunity will be gone tomorrow. They create a false sense of urgency so investors turn over money “right now,” without researching the investment. They may trick investors into believing that the investment “opportunity” is limited to a certain number of investors who can get in on it or has a deadline triggered by an event that will soon occur (Office of Investor Education and Advocacy, 2019).

Fake Testimonials - Con artists may pay people to post fake online reviews or appear in videos falsely claiming to have gotten rich from some investment opportunity. Even testimonials that appear to be independent and unbiased reviews – for example on a website purporting to “review” products and investment opportunities – may be part of the scam (Office of Investor Education and Advocacy, 2019).

Red flags in Payment Methods for Investments.

(Office of Investor Education and Advocacy, 2021)

Credit Cards - Most licensed and registered investment firms do not allow their customers to use credit cards to invest.

Digital Asset Wallets and “Cryptocurrencies.” - Licensed and registered financial firms typically do not require their customers to use digital asset wallets or digital assets, including so-called “cryptocurrencies,” to invest.

Wire Transfers and Checks - If you pay for an investment by wire transfer or check, be suspicious if you’re being asked to send or to make the payment out to a person or to a different firm, the address is suspicious (for example, an online search for the address suggests it is not an office building where the firm operates), or you are told to note that the payment is for a purpose unrelated to the investment (for example, medical expenses or a loan to a family member).

Alternative Ways to Invest

Depending on your circumstances, you may or may not have access to reliably investing in the ways mentioned above. Below is a list of common investments that you may also find helpful.

Foreign Currency Accounts: Some people opt to save in foreign currencies, which are often more stable than their local currency. They may open bank accounts denominated in US dollars, euros, or other stable currencies to protect their savings from inflation.

Precious Metals: Gold, silver, and other precious metals are traditional stores of value that are resistant to inflation. People may invest in these commodities or purchase jewelry as a way to safeguard their wealth.

Real Estate: Investing in real estate can be a hedge against inflation in developing countries. Property values tend to rise over time, providing a relatively stable store of wealth compared to cash. Additionally, rental income can provide a regular source of revenue.

Informal Savings Groups: In many developing countries, informal savings groups or rotating savings and credit associations (ROSCAs) are prevalent. Members contribute money to a common pool, which is then loaned out to members on a rotating basis. These groups provide a means of saving and accessing funds without relying on banks.

Digital Payments and Mobile Money: With the proliferation of mobile phones and digital payment platforms, many people in developing countries are turning to digital financial services to save and transfer money securely. Mobile money services allow individuals to store value digitally and conduct transactions without relying on physical cash.

Investments in Livestock or Agricultural Products: In rural areas, people may invest in livestock or agricultural products as a way to preserve wealth. These assets can provide a source of income through sales or breeding, and they are less susceptible to inflation than cash.

Microfinance and Savings Accounts: Microfinance institutions offer savings accounts and other financial services tailored to the needs of low-income individuals. These accounts often provide higher interest rates than traditional banks and may offer protection against inflation.

How does Investing impact your overall financial plan?

(ChatGPT, 2024)

Investing plays a crucial role in a financial plan, contributing to wealth accumulation, goal achievement, and long-term financial security. By strategically allocating funds to a diversified portfolio of assets such as stocks, bonds, and cash, you have the potential to generate returns that outpace inflation, ensuring the preservation and growth of your wealth over time. A well-thought-out investment strategy is tailored to your financial goals, risk tolerance, and time horizons, providing a foundation for building and sustaining wealth.

Investing serves as a means to achieve specific financial objectives, whether it's funding a comfortable retirement, purchasing a home, or funding a child's education. A carefully crafted investment plan considers factors such as risk tolerance and time horizon. Regular monitoring and adjustments to your investments can help adapt to changing market conditions and evolving financial goals. Ultimately, a thoughtfully integrated investment strategy forms a cornerstone of a financial plan, offering the potential for long-term financial growth and stability.

Prayerful Consideration

There are countless ways to invest. However, you may be limited in your available options because of where you live. Prayerfully consider how these principles can best be applied to your unique situation.

References

Calpers. (2023). How to Find a Trustworthy Financial Advisor. Perspective. https://news.calpers.ca.gov/how-to-find-a-trustworthy-financial-advisor/

ChatGPT (Version 3). (2024). [AI]. Open AI. https://chat.openai.com/auth/login

Hinckley, G. B. (2001). A Prophet’s Counsel and Prayer for Youth. Ensign.

Office of Investor Education and Advocacy. (2009, August 28). Beginners’ Guide to Asset Allocation, Diversification, and Rebalancing [..Gov]. U.S Securities and Exchange Commission. https://www.sec.gov/about/reports-publications/investor-publications/investor-pubs-asset-allocation

Office of Investor Education and Advocacy. (2019, June 26). How Fees and Expenses Affect Your Investment Portfolio [..Gov]. U.S Securities and Exchange Commission. https://www.sec.gov/investor/alerts/ib_fees_expenses.pdf

Office of Investor Education and Advocacy. (2019, October 10). Don’t Fall for an Investment Scam – Investor Alert [..Gov]. U.S Securities and Exchange Commission. https://www.sec.gov/oiea/investor-alerts-and-bulletins/ia_dontfallscam

Office of Investor Education and Advocacy. (2021, July 27). Fraudsters Posing as Brokers or Investment Advisers – Investor Alert [..Gov]. U.S Securities and Exchange Commission. https://www.sec.gov/oiea/investor-alerts-and-bulletins/ia_dontfallscam

Office of Investor Education and Advocacy Securities and Exchange Commission. (2015). Saving and Investing: A Roadmap to Your Financial Security Through Saving and Investing. https://www.sec.gov/pdf/facts.pdf

Perry, T. L. (1991). Becoming Self-Reliant. Ensign.

Schock, L. (n.d.). Don’t Panic, Plan It! [..Gov]. Investor.Gov. https://www.investor.gov/additional-resources/spotlight/directors-take/dont-panic-plan-it

The Church of Jesus Christ of Latter-day Saints. (2017). Learn—Maximum Time: 45 Minutes. In Personal Finances for Self-Reliance. https://www.churchofjesuschrist.org/manual/personal-finances-for-self-reliance/9-managing-financial-crises/learn-maximum-time-45-minutes?lang=eng

The Office of Financial Readiness. (2020). Basic Investing. In Touchdown Curriculum. https://finred.usalearning.gov/assets/downloads/Basic%20Investing.pdf

This content is provided to you freely by BYU-I Books.

Access it online or download it at https://books.byui.edu/fcs_340_readings/chapter_5_investing.